/feature

On Party Business

The Party shapes the game. Companies win it on merit.

Chuanwei is a Chinese billionaire. In his youth, his family was persecuted by the Communist Party for their political and class background. After China's economy opened up, he scraped together about $1,000 to start a small electronics company supplying wiring to factories in the booming southern industrial cities. Unable to convince investors to back a move into higher-tech renewable energy, he struck out on his own. With foreign direct investment from Germany, he began building a new company in a sector dominated by large state-owned enterprises. As he expanded, he raised capital from American and Singaporean private equity, and eventually listed the firm on the New York Stock Exchange. Despite discrimination from a state that prefers the companies it owns, he has built one of China's largest wind turbine manufacturers.

Mr. Zhang is also a Chinese billionaire. His first known job was as a clerk, then as a political officer, in a People's Liberation Army unit. He moved through the Party-state bureaucracy and into a role at a state-owned enterprise. With no formal engineering background, he leveraged those connections to run a joint venture between a Chinese state firm and a foreign partner manufacturing electrical equipment. When he later started his own business, he used his connections to get land rezoned, increasing its value by millions. His entry into wind power aligned with Beijing's push to scale up strategic industries. Today, his company expands into new sectors and foreign markets in line with Communist Party policy. He is also the Party Secretary of his own firm.

These two businessmen are, in fact, the same person. Zhang Chuanwei is the founder of Mingyang, China's second-largest and most innovative wind turbine company.1

To a Western reader, this combination of entrepreneurial risk-taker and Party insider may seem contradictory. But Zhang's CV is typical of his generation of Chinese business leaders, now in their late fifties and sixties. And for every generation of Chinese entrepreneurs, doing business in China means operating inside a system shaped by the Party. Chinese businesspeople may be businesspeople first, but they are always working within a political context the Party has created, and often directly embedded within it.

How the Party exerts influence

The Party influences companies both directly and indirectly. It does not usually micromanage firms. Instead, it defines the environment in which they succeed or fail—through capital allocation, market shaping, and the party cells embedded in every significant company.

Access to capital

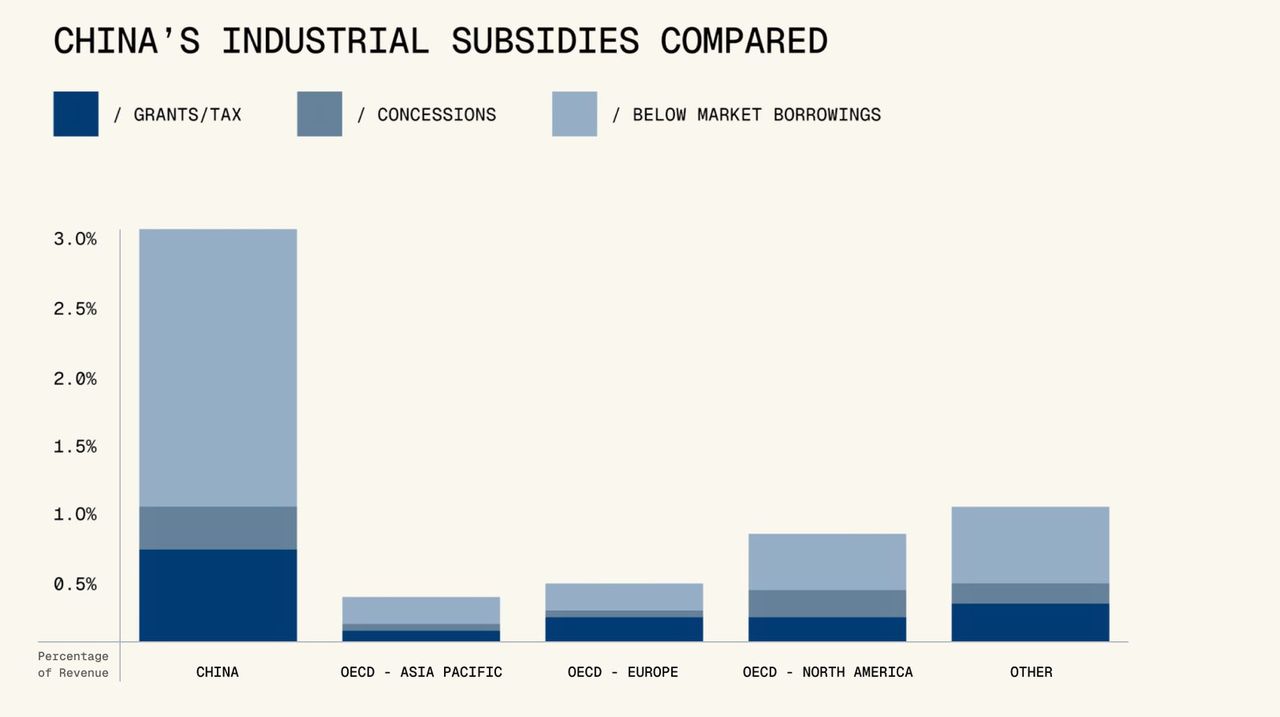

Capital allocation in China is not politically neutral. The large commercial banks are state-owned, and all banks operate under significant political direction. The clearest beneficiaries are state-owned enterprises. They are far less likely to have credit rationed, and have received more lending than their commercial performance would merit, before,2 during,3 and after4 the 2008 financial crisis. Some of this reflects state banks signalling alignment with political goals. Some of it is just commercial logic: why lend to a private firm that might fail when you can lend to a state enterprise that will almost certainly be bailed out? Just as how, in the West, no one ever got fired for buying IBM, no Chinese bank employee is ever reprimanded for lending to a state-owned enterprise.

State-owned companies do occasionally go bust, and regularly face restructuring. But the flow of credit to firms the Party considers strategically crucial is remarkably resilient. China First Heavy Industries has posted losses for three consecutive years, carries an asset-liability ratio of 86 percent5 against a manufacturing sector average of 57 percent,6 and is undergoing its fourth restructuring of this century. Its previous crisis, in 2015–2016, followed a corruption scandal that ended with its CEO taking his own life.7 A private firm in this condition would be bracing for collapse. China First Heavy Industries borrows at 3 to 4 percent and is going nowhere.

Large private firms that have established themselves as national champions also receive support, though the sequencing matters. Huawei is the best-documented case. As it grew from a major player in Chinese telecoms to a globally significant company across the 2000s and 2010s, it benefited from state-backed financing, often indirectly (usually through low-cost loans extended to its domestic and international customers to purchase Huawei equipment.) This was not support handed to an unproven startup. By the time Huawei received this kind of backing, it had already demonstrated it could compete globally.8 The Party was amplifying a winner, not picking one from scratch. For most Chinese firms—smaller, private, not yet proven at national scale—political alignment does not unlock preferential credit. The credit system rewards those who have already shown they matter.

Shaping the market

Credit allocation matters for big firms. But for firms of all sizes, it is the Party's market shaping that most determines which businesses thrive in China. This is where sensitivity to Party signals becomes not just helpful but essential.

Zhang Chuanwei did not decide to enter wind power in 2006 by accident. In 2005, Beijing mandated that all wind turbine projects use equipment with at least 70 percent domestic value added.9 Grid companies were required to purchase all renewable power produced, at guaranteed national prices.10 These rules did not hand Zhang a business; thousands of other entrepreneurs, backed by local governments across the country, rushed into the same space. But they created the conditions in which a business like his could be built. They also explain why the local government in Zhongshan was willing to rezone his land (from industrial to commercial, thereby increasing its value), effectively handing him a substantial subsidy. Backing a strong local company in a nationally strategic sector served the career interests of local officials as much as it served Zhang.

The subsidies did not last. Over the following years, grid purchase requirements were relaxed and price supports wound down.11 Most of Zhang's competitors went bust. Mingyang survived because it had become genuinely competitive during the years when the market was shaped to allow that. It began by acquiring intellectual property from Germany's Aerodyn; today it is expanding abroad using its own designs, refined over two decades of iteration. The Party created the game. Zhang won it on his own merits.

The same pattern ran through electric vehicles and batteries. From 2001, Beijing funded EV and hybrid research.13 From 2009, it began offering subsidies for domestic EV sales14 that increased over time, combined with local content requirements and rules obliging foreign firms to transfer technology to Chinese partners. Thousands of firms entered, state-owned and private alike. The subsidies were gradually withdrawn. Most firms failed. The biggest winners were CATL in batteries and BYD in vehicles—both originally private electronics companies that identified the EV opportunity early.

Both now play an outsized role in global supply chains in their respective sectors. They succeeded in intensely competitive markets. But those markets were created by the Party.

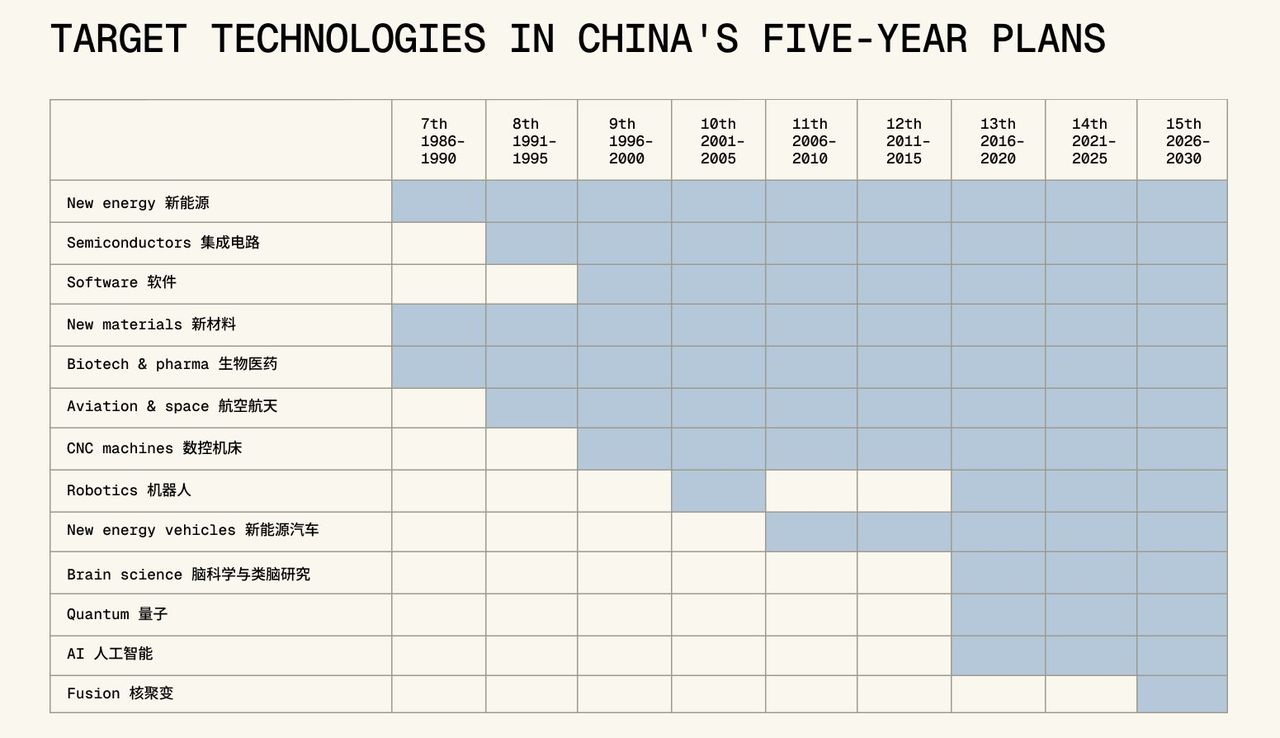

This is not random. Chinese leaders have declared the importance of technological development for decades,16 and Xi Jinping has described the high-tech sector as "the main battlefield" between superpowers.17 The Party has a clear plan, advancing through target technologies from new energy through semiconductors, EVs, robotics, AI, and quantum, with the five-year plans setting the cadence. The record is mixed—after forty years of effort, China still cannot sell a commercial airliner abroad, and the returns on decades of semiconductor investment remain uncertain. But in sectors where the playbook has worked, a handful of winners forged in brutal domestic competition now dominate global supply chains.

The Party cell

The Party's influence through capital and market shaping is structural and largely impersonal. It also has a more direct mechanism: the party cell embedded within firms themselves.

By law, any company with three or more Party members—roughly seven percent of China's population holds membership—is required to maintain a party committee. Before Xi Jinping, this was laxly enforced. Since his consolidation of power, it has become near-universal among significant firms. Officially, party committees transmit Party policy, conduct political education, and monitor alignment with central directives. In state-owned enterprises, and often in practice at large private ones, their remit extends to approving personnel appointments, major projects, and significant expenditure.

Direct evidence of party cells overriding commercial decisions at major private firms is limited. In part this is because it rarely needs to happen: when most of your senior leadership are Party members, they already know what the Party expects. At Mingyang, the point is made explicit; Zhang Chuanwei serves simultaneously as CEO and as head of the company's party committee. The cell is not the primary instrument of Party influence. But it is there, and it closes any remaining gap between the firm and the system it operates within.

Doing business with China

Western and East Asian firms that entered the Chinese market willingly and made enormous profits now complain about unfair Chinese competition. Firms like General Motors willingly shared electric vehicle technology with Chinese counterparts in the early 2010s. By 2023, the CTO of Ford was driving a Chinese electric car.18

But the firms now complaining had already made their choice, and the alternative was probably worse. When the Party identifies a sector as strategic and creates the conditions for Chinese firms to dominate it, staying out does not neutralise the threat. It only means losing the ability to shape how it affects you.

In 2011, Elon Musk dismissed BYD by asking, "Have you seen their cars?"19 Today BYD is the largest electric vehicle manufacturer in the world, and nearly half of Tesla's vehicles are made in China.20 Volkswagen initially came to China for cheap manufacturing and market access. Now it treats China as essential to staying at the cutting edge of the industry, investing heavily in its innovation centre in Hefei.21 It has become so integrated into the Chinese EV ecosystem that it is now a target of EU tariffs on Chinese-made vehicles.22

Rejecting engagement with the Party would once "just" have meant absence from Chinese markets and inability to access Chinese supply chains. Now, at least in electric vehicles, it means absence from the frontier.

That will not be true in every sector. The Party's backing is not a guarantee of success. But its planners have shown they can create world-leading industries through sustained political commitment, and they have shown it in the sectors—clean energy, batteries, electric vehicles—that sit at the centre of the twenty-first-century economy. For firms in those industries, not engaging with China is not a neutral choice. It is a decision to cede the frontier.

Recognising this, however, does not mean rushing in. It does mean understanding the political context as well as the commercial one. Markets operate, firms compete, and entrepreneurs succeed. But they do so within a framework the Party defines. Whatever you believe about the interests of your company or your Chinese partner, the Party's interest will always come first.

- 1Qiu Xiaofen, 炒地皮发家,一顿饭价值百万,风电巨头「明阳智能」资本变形计, 36Kr, April 8, 2022, https://36kr.com/p/1678137976759305; and "捕风汉子张传卫:倚仗财技夹缝求生," 北极星风力发电网, March 31, 2011, https://news.bjx.com.cn/html/20110331/276242.shtml.

- 2"State Ownership and Credit Rationing: Evidence from China," ScienceDirect, https://www.sciencedirect.com/science/article/abs/pii/S105905602300182X.

- 3Han Gao, Jie Li, Fang Liu, and Jin Wu, "State Ownership and Credit Rationing: Evidence from China," International Review of Economics & Finance 88 (2023): 237–257, https://doi.org/10.1016/j.iref.2023.06.014; and Jialin Gong, "Biased Bank Loan Expansion and Firm Political Connection: Evidence from China's 2009 Stimulus Program," 2024, https://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2024-Lisbon/papers/BiasedBankLoanandFirmPoliticalConnection_JialinGong.pdf.

- 4Xiaoming Li, Zheng Liu, Yuchao Peng, and Zhiwei Xu, "Bank Risk-Taking, Credit Allocation, and Monetary Policy Transmission: Evidence from China," Federal Reserve Bank of San Francisco Working Paper Series, October 2024, https://www.frbsf.org/wp-content/uploads/wp2020-27.pdf.

- 5连云快讯, "中国一重(601106.SH):2024年年报净利润为-37.36亿元,同比亏损扩大," 界面新闻, April 30, 2025, https://m.jiemian.com/article/12717472.html.

- 6国家统计局, "2025年全国规模以上工业企业利润增长0.6%," January 27, 2026, https://www.stats.gov.cn/sj/zxfb/202601/t20260127_1962382.html.

- 7Reuters, "China's First Heavy Chairman Commits Suicide amid Anti-Graft Probe," August 4, 2015, https://www.reuters.com/article/world/china-s-first-heavy-chairman-commits-suicide-amid-anti-graft-probe-xinhua-idUSKCN0Q90SJ/.

- 8Eva Dou, House of Huawei: The Secret History of China's Most Powerful Company (New York: Portfolio, 2025).

- 9National Development and Reform Commission, "关于风电建设管理有关要求的通知," Energy Development and Reform No. 1204, July 4, 2005, https://www.ndrc.gov.cn/xxgk/zcfb/tz/200508/t20050810_965825.html.

- 10State Electricity Regulatory Commission, "Measures for the Supervision of the Full Purchase of Renewable Energy Electricity by Power Grid Enterprises," https://fjb.nea.gov.cn/dtyw/jgdt/202311/t20231110_198995.html.

- 11National Development and Reform Commission, "关于完善风电上网电价政策的通知(发改价格〔2019〕882号)," https://www.ndrc.gov.cn/xxgk/zcfb/tz/201905/t20190524_962453.html; and "国家发展改革委关于2021年新能源上网电价政策有关事项的通知," https://www.gov.cn/zhengce/zhengceku/2021-06-11/content_5617297.htm.

- 12How governments back the largest manufacturing firms (EN).

- 13"国家'863'计划电动汽车重大专项已启动," Sina Auto, September 30, 2001, https://auto.sina.com.cn/news/2001-09-30/14521.shtml.

- 14Ministry of Finance, "Notice on Carrying Out Pilot Work on the Demonstration and Promotion of Energy-Saving and New Energy Vehicles," February 10, 2009, https://www.mof.gov.cn/gp/xxgkml/jjjss/200902/t20090210_2499581.htm.

- 15Chart adapted from Kyle Chan, "China's Technology Long Game," High Capacity, https://www.highcapacity.org/p/chinas-tech-long-game.

- 16Deng Xiaoping, "Speech at the Opening Ceremony of the National Conference on Science," 1978, https://www.marxists.org/reference/archive/deng-xiaoping/1978/30.htm.

- 17"Xi Jinping Calls for Chinese Scientists to Step Up Innovation in Hi-Tech 'Battlefield,'" South China Morning Post, https://www.scmp.com/news/china/politics/article/3267982/xi-jinping-calls-chinese-scientists-step-innovation-hi-tech-battlefield.

- 18Kyle Chan, "China's Faustian Bargain for Foreign Firms," High Capacity, https://substack.com/@kyleichan/p-156884861.

- 19"Tesla's Musk Laughs at BYD," Bloomberg, https://www.youtube.com/watch?v=_9ftbRWqkjo.

- 20"Tesla Shanghai Gigafactory Produces 4 Millionth Vehicle amid Slight Production Slowdown," CarNewsChina, December 8, 2025, https://carnewschina.com/2025/12/08/tesla-shanghai-gigafactory-produces-4-millionth-vehicle-amid-slight-production-slowdown/.

- 21Volkswagen Group, "Test Center Complete: Volkswagen Group Now Able to Fully Develop and Validate Products in China for China," https://www.volkswagen-group.com/en/press-releases/test-center-complete-volkswagen-group-now-able-to-fully-develop-and-validate-products-in-china-for-china-20009.

- 22"EU to Review Tariffs on Volkswagen's EVs Made in China," Financial Times, https://www.ft.com/content/675d3729-972b-4f35-9daf-5dc2c1d1f480.

- 29Qin Shi Huang, First Emperor of China, The British Library, via Wikimedia Commons.

- 30The Thirteen Factories, Guangzhou, via Wikimedia Commons.

- 31Bamboo, Kuang Xü after Cheng Banzhao, Museum Collection.

About the author

Michael Hill /@Michael_J_Hill

Michael Hill is a policy researcher at Britain Remade, a pro-growth campaigning organisation. He previously worked at the UK government's Department of Energy, where he advised the government and business on the national security implications of procuring equipment from China and partnering with Chinese companies. Before that he was a journalist based in Northeast China. You can find him on X at @Michael_J_Hill.